Understanding Cross Border Payments

Cross-border payments move money across countries through multiple banks, networks, and compliance layers. Here’s how they work, and why modern payment infrastructure matters.

- Remove the current class from the content27_link item as Webflows native current state will automatically be applied.

- To add interactions which automatically expand and collapse sections in the table of contents select the content27_h-trigger element, add an element trigger and select Mouse click (tap)

- For the 1st click select the custom animation Content 27 table of contents [Expand] and for the 2nd click select the custom animation Content 27 table of contents [Collapse].

- In the Trigger Settings, deselect all checkboxes other than Desktop and above. This disables the interaction on tablet and below to prevent bugs when scrolling.

Cross-border payments are the backbone of modern global commerce. As businesses expand internationally, they must move money across currencies, jurisdictions, and banking systems-reliably, quickly, and at scale.

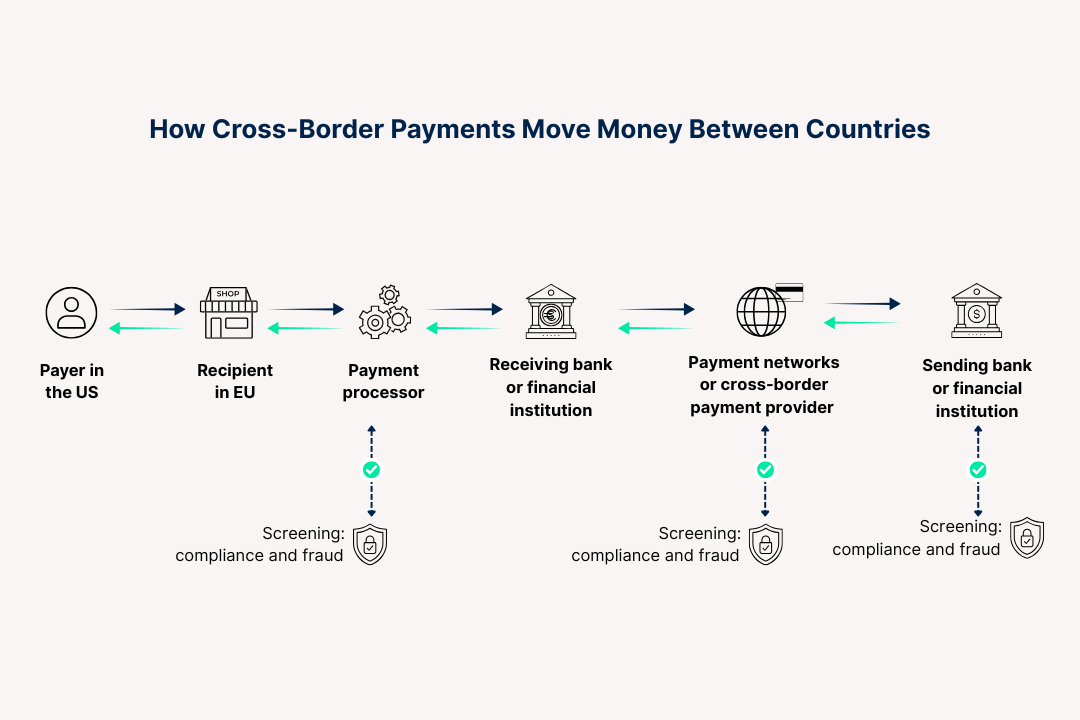

What actually moves when money crosses a border

A cross-border payment is more than one bank sending funds to another. It is a choreography of messaging, compliance checks, foreign exchange conversion, and settlement across different legal and technical systems.

Two threads move in parallel. The first is information: a payment message travels through one or more networks that carry data about who sends, who receives, and why. The second is value: money shifts between accounts at banks, often through pre-funded nostro accounts or central-bank real-time gross settlement systems.

Because banks in different countries rarely hold direct accounts with each other, transfers often pass through correspondent banks. Each stop can add a fee, a format change, and a new round of compliance screening. The result can be slow, opaque, and occasionally error-prone.

Sometimes the funds also convert from one currency to another. That FX leg introduces a new source of cost and risk. Rate moves while payments are in-flight can change the amount the receiver gets.

Cross-Border Payment Methods

A payment becomes cross-border when the sender and the recipient are based in different countries, regardless of how the funds are transferred. Choosing the right payment method for an international transaction depends on several variables, including the transaction value, required settlement speed, currencies involved, and the total cost of processing the payment.

Both businesses and individuals making cross-border payments should evaluate the available payment options carefully and select the method that best aligns with their operational needs, cost expectations, and customer experience requirements.

Below are some of the most widely used cross-border payment methods:

Wire Transfers

Wire transfers involve the electronic movement of funds between banks or financial institutions across borders. Different regions rely on different wire networks, each serving specific geographic areas. Wire transfers are typically used for high-value transactions and can support multiple currencies, though processing times and fees vary by country and banking network.

Credit Card Payments

Credit cards are accepted globally, allowing businesses to collect payments from international customers with minimal friction. While they offer convenience and broad reach, cross-border card payments often incur currency conversion costs and additional international processing fees.

Electronic Funds Transfers (EFTs)

Electronic funds transfers-also known as electronic bank transfers or e-payments, enable fast and secure money movement directly between bank accounts. Compared to traditional wire transfers, EFTs are generally quicker, easier to initiate, and more cost-efficient for many cross-border use cases.

International Money Orders

International money orders are a more traditional, paper-based payment option that can be mailed or processed electronically via third-party providers. Available through banks and financial institutions, they are usually used for smaller payment amounts and specific use cases where digital options may not be accessible.

Online Payment Platforms

Online payment platforms allow users to send and receive international payments through web or mobile interfaces. These platforms often provide competitive exchange rates and lower fees, making them attractive for both consumers and businesses. Many global card networks also enable cross-border payments through online channels.

Cryptocurrencies and Stablecoins

Digital assets such as USDC and EURC, as well as cryptocurrencies like Bitcoin and Ethereum, can be used for international payments without relying on traditional banking intermediaries. These transactions can settle quickly and securely across borders. While regulatory requirements and price volatility remain important considerations, stablecoin payments in particular are now being adopted at scale, with retailers integrating them into live payment operations rather than limiting them to pilot programs.

What Are Cross-Border Payments Used For?

Cross-border payments are a foundational part of the global economy, enabling money to move between countries for both business and personal purposes. As digital services and global commerce continue to expand, these payments support a wide range of use cases across industries and regions.

Common applications of cross-border payments include:

International Trade

Businesses involved in global trade rely on cross-border payments to pay international suppliers, settle invoices, and receive funds from customers in foreign markets. Efficient cross-border payments are essential for maintaining cash flow and supporting international expansion.

Travel and Tourism

Cross-border payments power the global travel ecosystem, allowing travellers to pay for flights, accommodation, car rentals, and experiences abroad. They also enable travel platforms, airlines, hotels, and tour operators to settle funds efficiently across borders.

Marketplaces and Digital Platforms

Online marketplaces and digital platforms use cross-border payments to collect funds from buyers and distribute payouts to sellers, partners, and service providers in different countries. These payment flows often involve multiple currencies and require fast, transparent settlement.

Fintech and Financial Services

Fintech platforms depend on cross-border payments to support international account funding, money transfers, treasury operations, and customer withdrawals. Reliable global payment infrastructure is critical for scaling financial services across markets.

Trading Platforms

Trading platforms use cross-border payments to enable international account funding, asset settlement, and user withdrawals. These payment flows support participation across jurisdictions and currencies while requiring speed, security, and regulatory compliance.

Gaming Platforms

Gaming platforms rely on cross-border payments to accept player deposits, process payouts, and monetize digital content for users worldwide. Global reach and seamless payment experiences are essential for player engagement and platform growth.

Remittances

Individuals use cross-border payments to send money to family members and friends in other countries. These transfers play a vital role in supporting households and communities, particularly in emerging economies.

Investment

Cross-border payments enable investors to move capital internationally to purchase assets, manage portfolios, and receive returns from global investments.

International Donations and Aid

Charitable organisations and donors rely on cross-border payments to fund humanitarian aid, nonprofit initiatives, and social programs across borders, supporting causes and communities around the world.

Benefits and Challenges of Cross-Border Payments

Cross-border payments open powerful opportunities for businesses to scale internationally, access new markets, and unlock additional revenue streams, often with greater speed and efficiency than traditional expansion models. At the same time, operating across borders introduces regulatory, financial, and operational complexities that must be carefully managed.

Below is an overview of the key benefits and challenges associated with cross-border payments.

Benefits

Access to Global Markets

Cross-border payments enable businesses to operate beyond domestic boundaries, connecting with international customers, suppliers, and partners. This global reach is essential for companies looking to expand their footprint and compete internationally.

Revenue Growth Opportunities

By selling products and services across borders, businesses can unlock new sources of revenue and accelerate growth. International demand often provides opportunities that may not exist in local markets.

Business Diversification

International payment capabilities allow businesses to diversify their customer base, supply chains, and investment exposure. This reduces dependence on a single market and helps mitigate regional economic risks.

Potential Cost Efficiency

Certain cross-border payment methods can reduce costs related to transaction fees, currency conversion, and intermediaries. Optimizing payment routes can lead to meaningful savings, particularly for high-volume or recurring transactions.

Payment Flexibility

Cross-border payments give businesses the ability to choose from multiple payment methods and currencies, allowing them to tailor payment flows to specific markets, partners, and operational needs.

Challenges

Regulatory and Compliance Complexity

Cross-border payments are subject to varying regulations, licensing requirements, and compliance standards across jurisdictions. Managing these obligations requires robust controls and ongoing oversight.

Currency Exposure

Fluctuations in exchange rates can affect transaction values and cash flow. Without proper FX management, currency volatility can introduce financial uncertainty.

Fees and Cost Variability

Fees for cross-border payments can differ significantly depending on the payment method, currency pair, and region involved. Lack of transparency can make cost management difficult.

Fraud and Security Risks

International payments can be exposed to risks such as fraud, cyber threats, identity theft, and payment scams. Strong security measures are essential to protect funds and sensitive data.

Operational Complexity

Compared to domestic transactions, cross-border payments often involve additional steps, reconciliation processes, and coordination across systems. Businesses need the right infrastructure and expertise to manage these operations efficiently.

Why it still feels hard

Most of the friction comes from five intertwined issues. Each one is solvable, but not by a single switch flip.

- Interoperability: hundreds of local payment schemes, differing formats and rules, and staggered adoption of modern messaging standards make straight-through processing difficult.

- FX risk: volatile exchange rates and wide spreads, especially on exotic corridors or outside market hours, can erode value.

- Regulation and compliance: each jurisdiction applies its own KYC, sanctions, and data-sharing rules; the same payment can be checked several times along its route.

- Processing delays: batch windows, time-zone gaps, manual reviews, and missing data stall transactions.

- Fraud and cyber risk: long chains with inconsistent controls invite abuse and force banks to add layers of monitoring.

- Transparency: hidden markups and unclear fees make it hard to know the true total cost.

Small shifts on any one of these factors can speed or stall a transfer. When two or three hit at once, payments back up and reconciliation piles up on the finance team’s desk.

How to Send Cross-Border Payments

Sending money across borders requires thoughtful preparation and accurate execution. Working with a payment provider that understands your business, your accounts, and the countries you operate in can significantly simplify the process. Selecting the appropriate payment method and validating all transaction details helps ensure payments are completed efficiently, accurately, and securely.

While the exact steps may vary depending on the countries involved and the payment rail used, the core process generally follows these stages:

1. Select the Appropriate Payment Method

There are several options for sending cross-border payments, including bank transfers, card payments, electronic transfers, online payment platforms, and digital assets. Each method differs in terms of speed, cost, currency support, and settlement time, so it’s important to choose the option that best fits the transaction size, urgency, and destination.

2. Review the Exchange Rate

When a payment involves currency conversion, reviewing the applicable exchange rate is essential. Understanding how the rate affects both the total cost and the final amount received helps avoid surprises and supports better cash flow planning. Exchange rates may vary depending on the payment method and the countries involved.

3. Enter Recipient Information

To process a cross-border payment, accurate recipient details are required. This typically includes the recipient’s name, bank or account information, and routing or identification codes. In some cases, additional data such as payment purpose or reference numbers may be needed, depending on local regulations and transfer networks.

4. Confirm Payment Details

Before submitting the payment, all information should be carefully reviewed. Verifying amounts, currencies, and recipient data helps prevent errors, delays, or failed transactions—especially when using payment methods that cannot be reversed once processed.

5. Initiate the Transfer

Once confirmed, the payment can be sent using the selected method. Settlement times vary depending on the payment rail, currencies, and destination countries, ranging from near-instant to several business days.

6. Monitor the Transaction

Tracking cross-border payments provides visibility and assurance that funds have reached the intended recipient. Most payment providers offer reference numbers or tracking tools that allow businesses and individuals to monitor payment status from initiation to completion.

Cross-Border Payments With Yugo

Yugo replaces fragmented international payment chains with a single, multi-rail payment infrastructure built for global operations. Instead of relying on multiple providers or region-specific solutions, Yugo intelligently orchestrates payment rails to route each transaction through the most cost-effective and efficient path, automatically and compliantly, all through one API and one operational framework.

Payment Rails Supported by Yugo

Yugo supports multiple payment rails and orchestrates between them based on geography, currency, fees, and settlement speed-ensuring optimal cost and performance for every transaction:

- Bank Transfers (A2A / Open Banking): Direct account-to-account payments with cost-effective fees, ideal for high-value and B2B transactions.

- Stablecoins: Near-instant cross-border settlement with reduced intermediary and FX costs, well-suited for treasury operations, payouts, and international settlements.

- Cards: Globally accepted and familiar to end users, supporting consumer-facing payment flows where convenience and reach are key.

- Alternative Payment Methods (APMs): Local payment options that improve regional conversion rates and lower overall payment costs by reducing reliance on cards.

All rails are unified into a single system, allowing businesses to optimize costs without managing multiple providers. One API. Any rail. Anywhere.

Currency Conversion and FX

Currency exchange is one of the largest hidden costs in cross-border payments. Yugo reduces FX friction by automating currency routing, supporting multi-currency balances, and minimizing unnecessary conversions. Clear visibility into rates and fees helps businesses control costs while settling in the currency that best fits their operations.

Settlement Speed and Cash Flow

Traditional cross-border payments can take days to settle, tying up capital and increasing operational risk. Yugo shortens settlement cycles-particularly through stablecoin rails-providing faster access to funds, improved liquidity, and more predictable cash flow for global businesses.

Compliance and Security

Yugo embeds compliance and security directly into the payment infrastructure. AML and KYC controls, transaction monitoring, and secure fund handling across all rails enable businesses to operate globally while meeting regulatory requirements, without adding operational overhead or market-by-market complexity.

Who Benefits from Yugo’s Cross-Border Payments?

Yugo supports cost-conscious, globally active businesses, including marketplaces, travel platforms and OTAs (Online Travel Agencies) , fintech companies, digital platforms, SaaS providers, Web3-enabled businesses, and enterprises with international suppliers or customers.

Why Businesses Choose Yugo

Yugo turns cross-border payment complexity into a cost-efficient, orchestrated infrastructure. With one API, businesses access multiple rails, intelligent routing, faster settlement, lower transaction and FX costs, transparent reporting, and a compliance-first, enterprise-ready architecture-replacing fragmented payment stacks with a single global payments backbone.